Military Conflicts and Global Stock Returns

Key Takeaways

Military conflicts are not new to markets, and historical data shows stocks have navigated many such periods over time.

Market reactions to conflicts have varied in the short term, while longer horizons often look different than initial headlines suggest.

Global market data suggests that conflict-related volatility has not been limited to any single region.

What Happens After Conflict Begins? Start With the Data

As markets closed in the U.S. on the last trading day of February 2026, year-to-date stock market returns ranged from middling — the S&P 500® Index was up ~0.7% — to very strong — the MSCI Emerging Markets IMI Index was up nearly 14.5% in U.S. dollar terms.

Over the weekend, geopolitical tensions in the Middle East spiked as the U.S. and Israel launched a series of coordinated strikes on Iran, with Iran responding and launching attacks at facilities in many neighboring countries.

Although the conflict has so far been limited to the region, concerns remain about its potential impact on oil supplies and energy prices, as well as downstream effects on production and supply chains. While uncertainty remains high and the ultimate effects are still unclear, it’s important to remember that markets are no stranger to conflict.

There is nearly 100 years of data on the U.S. stock market, covering many episodes of geopolitical unrest. This offers a rich history we can analyze to understand stock performance after the start of militarized conflicts.

In Figure 1, we examine the returns of U.S. stocks following major global events over the last 100 years. Returns are computed for three months, one year and three years after each event (starting with the first full month after each episode).

Figure 1 | U.S. Stocks Have Shown More Volatility in the Short-Term but Resilience Over the Longer Term Following Major Conflicts

Data from July 1926 – December 2025. Source: Ken French Data Library. Returns greater than one year are annualized. Past performance is no guarantee of future results.

The results provide important takeaways. Regardless of the time horizon, we observe more positive than negative market returns. Following major geopolitical events, it is likely that markets may be more volatile in the short term as uncertainty rises and new information is quickly reflected in prices, but that doesn’t guarantee markets will decline even three months out.

It’s important to note that the effects on prices around new conflicts aren’t solely due to the conflicts themselves. Other externalities exist that are also being considered by markets. Additionally, economic conditions at the time may influence the outcomes.

If a new conflict arises that affects the global economy during a period of already weak economic conditions (for example, around the 1973 oil embargo, which followed a recession just a few years earlier), that will certainly have impacted subsequent realized returns.

But importantly, as the time horizon extends beyond major conflicts, the likelihood of positive market returns increases. Notably, there were no negative returns in any of the three-year periods following the conflicts examined, and the average of the 3-year annualized returns in the sample was about 13%.

As time goes on, event-driven uncertainty often subsides, and investors who remain disciplined are typically rewarded for staying the course.

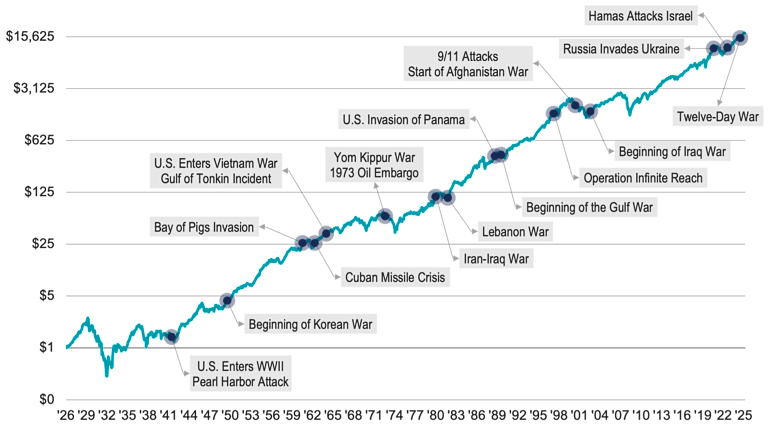

This key point is further demonstrated in Figure 2, which highlights the conflicts examined in Figure 1 against the long-term growth of 1 U.S. dollar since 1926. This visualization emphasizes the market's resilience over the long term despite numerous wars and military actions throughout history.

Figure 2 | With Military Conflicts, Long-Term Discipline Is Key for Investors

Data from July 1926 – December 2025. Source: Ken French Data Library. Past performance is no guarantee of future results.

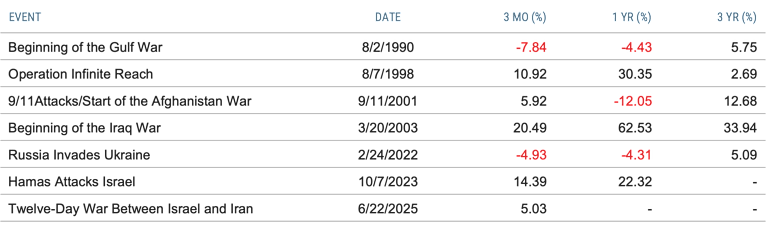

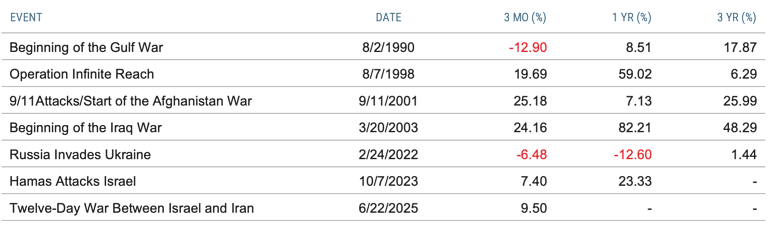

Do Global Markets React Similarly After Conflicts Begin?

Outside the U.S., markets have shown similar patterns around conflicts. There is generally less historical return data for non-U.S. markets, but within a smaller sample, we observe the same key points.

In Figure 3, we present returns for non-U.S. developed (Panel A) and emerging markets (Panel B) stocks following the events examined in Figure 1, starting in 1990. Just as in the U.S., we see greater near-term variation in outcomes after conflicts begin, but the three-year return after each event is again positive in all cases. The importance of discipline is well-supported across markets.

Figure 3 | Non-U.S. Stocks, Like the U.S., Have Benefited Investors Who Stay the Course Through Geopolitical Conflicts

Data from July 1990 – December 2025. Source: Ken French Data Library. Returns greater than one year are annualized. Past performance is no guarantee of future results.

We recognize that investors are human and have emotions, and events like military actions can evoke strong feelings. That’s natural.

However, for investors, allowing emotion or anxiety about the events of the world to drive meaningful asset allocation changes is not something that’s supported by historical data. Instead, it offers strong evidence that sticking to your financial plan is likely the prudent course of action during these times.

Explore More Insights

Glossary

Captures large, mid and small cap representation across emerging markets countries, covering approximately 99% of the free float-adjusted market capitalization in each country.

A market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. The index is widely regarded as the best gauge of large-cap U.S. equities.

International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

The opinions expressed are those of the investment portfolio team and are no guarantee of the future performance of any Avantis Investors portfolio.