ETFs – An Important Tool for Wealth Management

Since their creation in 1990 in Canada and 1993 in the U.S., exchange-traded funds (ETFs) have become widely used to help investors achieve their financial goals. Drawn by low turnover, lower fees, broad diversification and greater tax efficiency, investors have voted with their wallets, pouring more than $5 trillion into ETFs globally.¹

In this article, we discuss the growing appeal of ETFs and summarize the different types available to investors. We also review key differences between ETFs and mutual funds and offer some considerations for trading ETFs. While we believe both vehicles are effective for investors seeking to build long-term asset allocations, we think it is critical to understand key similarities and differences to help inform both asset allocation and asset location.²

ETF Usage is Growing

ETF growth has accelerated over the last 20 years. In 2000, U.S. ETFs held $66 billion in assets under management (AUM) compared to $5.1 trillion in long-term mutual funds. By the end of 2018, ETF assets in the U.S. had grown more than 50 times to $3.4 trillion, far exceeding the growth of mutual fund assets which had reached $14.7 trillion.³

Advisor adoption has been an important driver of ETF growth. In their 2018 Trends in Investing Survey, the Journal of Financial Planning and the FPA Research and Practice Institute™ reported that 87% of advisors surveyed use or recommend ETFs for clients while 73% use or recommend mutual funds (non-wrap). This represents the widest gap between ETF and long-term mutual fund usage reported since ETFs overtook mutual funds in the 2015 study.

We are also seeing significant interest in ETFs among higher income investors. According to the Investment Company Institute (ICI), households owning ETFs in non-retirement accounts tend to have higher incomes than households holding mutual funds.⁴ ICI reports that 57% of the households holding ETFs in taxable accounts reported income greater than $100,000 versus 45% in the case of households holding mutual funds. We believe higher income investors are attracted to the tax efficiency of ETFs.

Types of ETFs

Passive ETFs

Like index funds, passive ETFs seek to track the performance of indices. They can range from widely followed indices, such as the S&P 500® Index, to narrower indices such as a specific sector, country, or one created with specific exclusions. While ETFs tracking broadly held indices are offered by multiple providers, ETFs tracking more specialized indices are available from a few or even a single provider. Rebalancing in the indices these ETFs track typically occurs on a periodic basis. For example, the Russell 2000® Index rebalances once per year in June.

Strategic Beta ETFs

This type of ETF was introduced in 2006. They track the performance of indices that deviate from market capitalization with the objective of outperforming markets using a rules-based approach. Rebalancing is carried out periodically, similar to passive indexing strategies. As of December 2018, Morningstar reported that there were about 700 strategic beta exchange-traded products in the U.S. with $705 billion in AUM. The multifactor category is the most common with 171 products, while the value strategies with $177 billion were the most popular, closely followed by growth with $169 billion, when measured by AUM.⁵

Active ETFs

Active ETFs seek to add value like an actively managed mutual fund. Like actively managed mutual funds, active ETFs do not replicate a benchmark. Rather, managers have more discretion over when and how rebalancing occurs and are able to use their expertise with the goal of adding value for their clients. There are two structures in active ETFs:

the fully transparent active ETF that discloses holdings daily and

the non-transparent active ETF expected to arrive soon to the market.

Fully transparent ETFs help investors gain more transparency so that they can evaluate the implications of current holdings in the context of their overall portfolio design.

Mutual Funds and ETFs

Both mutual funds and ETFs are effective tools for helping investors build globally diversified portfolios. Both instruments are managed professionally, and regulated entities serve as custodians of their assets.

Mutual fund investors generally buy shares at the fund's net asset value (NAV) with cash. Similarly, redemptions are transacted at NAV with the fund transferring the proceeds to the redeeming investors the morning after the redemption. Portfolio managers receive the exact amount of net purchases and redemptions from all shareholder activity at the previous evening's NAV the morning after those transactions are executed. If the fund has a net purchase, portfolio managers may invest the cash and all shareholders bear the investment costs. If, on the other hand, there is a net redemption, the fund must transfer cash to the redeeming shareholders.

And, since the redeeming investors are no longer part of the fund, the costs of raising the cash are not borne by them, but by the remaining shareholders in the fund. These expenses could include transaction costs or borrowing costs if the fund borrows money to cover the transfer while portfolio managers sell securities to cover the cash shortfall.

Redeeming shareholders may also saddle remaining shareholders with a higher tax burden. When portfolio managers sell securities to satisfy redemptions, they may realize capital gains that must be distributed to the remaining shareholders at the end of the year. The higher tax awareness of some investors and the availability of tools to efficiently harvest losses in times when the market moves down can create challenging situations for fund managers. Loss harvesting flows tend to be correlated since they are driven by the same signal, a dip in the market, exacerbating the challenge.

Typical Interaction of Investors with Mutual Funds

Investors buy shares with and sell shares for cash.

Portfolio managers need to buy or sell securities to invest or deliver cash after the shareholders’ activity (fund may need loans).

Cost of buying or selling happens inside the fund.

Shareholders who sell do not incur cost of raising cash inside the fund.

Selling appreciated securities causes capital gains to be distributed to investors in the fund.

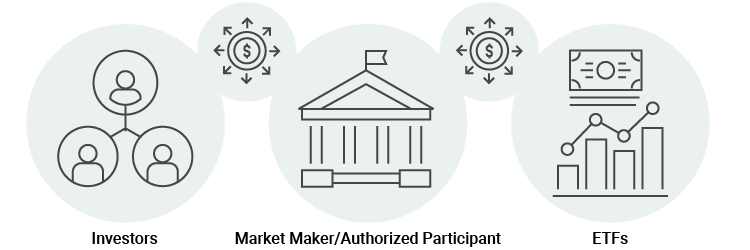

ETFs offer a more modern structure. They are listed on stock exchanges, allowing investors to buy and sell shares directly in the market. Like stocks, trades in ETFs are facilitated by market makers that provide liquidity in the marketplace by fulfilling buy and sell orders. If the market maker does not have enough shares to fill a buy order, it may create more ETF shares by delivering a basket of securities to the fund manager in exchange for ETF shares. Similarly, for sell orders, the market maker can deliver excess ETF shares to the custodian and receive a basket of securities, which can then be liquidated in the secondary market. Interactions between market makers and ETF managers happen at end-of-day NAV prices. Creating or redeeming ETF units in exchange for underlying securities is called the in-kind process which helps keep ETF market prices close to the NAV of the ETF.

In-kind transactions between the ETF and the market makers help shield investors from costs triggered by the activity of other shareholders. They also minimize the need for the ETF manager to hold or borrow cash because the interaction with market markers involves securities. An additional interesting feature of the in-kind redemption process is that it minimizes the need to sell securities and realize capital gains, which may help reduce year-end capital gain distributions.

Who pays for the shareholder activity costs? In in-kind transactions, the investors generating the activity pay the costs. Investors can buy ETF shares in market transactions at the ask price, which is the price market makers are asking for when selling the shares to investors. They can sell ETF shares at the bid price. The difference between the bid and ask prices is the spread, which reflects the spread of the basket of securities the market maker needs to deliver or accept from the ETF when creating or redeeming ETF shares.

Typical Interaction of Investors with ETFs

Investors buy and sell shares in the market. Bid-ask spreads reflect cost associated with transacting with the ETF.

Net transaction goes to authorized participant.

Portfolio managers receive or deliver baskets of securities in-kind to deal with shareholders' activity.

Portfolio managers tend to deliver low-cost basis stocks in-kind, keeping higher cost basis stocks in the ETF and minimizing unrealized capital gains inside the ETF.

ETFs are structured such that shareholders interacting with the ETF bear the costs of buying and selling.

Shareholders do not incur cost or capital gains realizations because in-kind activity minimizes the need to raise cash inside the ETF.

Trading ETFs

ETFs trade like other securities, with investors placing buy or sell orders through their brokers. Though placing orders in the market, particularly large orders, can create anxiety, investors have several tools at their disposal. First is the ability to trade with limit orders. These orders limit the price an investor is willing to pay when buying or to accept when selling. In addition, brokerage houses such as Fidelity, Schwab, TD and LPL offer specialized trading desks to help investors trade ETFs. These desks have professional traders who seek best execution through competitive bids from market makers.

Trading through a brokerage house desk allows investors to reach additional layers of liquidity. One layer includes the volume and the bid-ask spreads of the ETF shares quoted in the secondary market. Another layer is represented by the liquidity of the underlying basket of securities. When quoting ETF prices in competition, market makers look at both layers of liquidity to provide competitive quotes. Therefore, interacting with the specialized trading desks provides access to professional traders working to help achieve best execution.

Conclusion

- Funds and ETFs provide investors the ability to create globally diversified asset allocations. Both vehicles can help investors achieve their goals.

- ETFs offer some benefits relative to mutual funds, particularly for taxable investors. We believe this is a driver behind their growth. This relatively new investment vehicle helps investors minimize transaction costs and taxable distributions. The in-kind redemption process reduces the effect of near-term shareholder activity on long-term investors.

- Trading ETFs in the market may seem daunting at first, but brokerage houses have created tools and specialized desks to help investors improve the experience of buying and selling ETFs shares.

ENDNOTES

¹ETFGI. "ETFGI Reports Assets Invested in Global ETF and ETP Industry Reached a Record US$5.32 Trillion at the End of February 2019." Press Release. March 12, 2019.

²Morningstar Manager Research. Measuring ETFs' Tax Efficiency Versus Mutual Funds. Aug. 1, 2019. Morningstar's Ben Johnson, Director of Global Research, and Alex Bryan, Director of Passive Strategies Research, offered a more comprehensive comparison earlier in 2019.

³Investment Company Institute. Chapter Two, US-Registered Investment Companies. 2019 Investment Company Fact Book.

⁴Investment Company Institute and Strategic Business Insights. A Close Look at ETF Households. September 2018.

⁵Morningstar Manager Research. A Global Guide to Strategic-Beta Exchange-Traded Products. March 2019.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

The information in this document does not represent a recommendation to buy, sell or hold security. The trading techniques offered in this report do not guarantee best execution or pricing.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

GLOSSARY

Bid/ask spread. The bid price is the highest price that a buyer is willing to pay for the ETF. The ask (or offer) is the lowest price a seller is willing to accept for the ETF. The bid/ask spread represents the difference between the two prices.

Exchange-traded fund (ETF). Similar to a mutual fund, an ETF represents a group of securities, but the ETF trades on an exchange like an individual stock. An ETF generally follows the performance of an index, such as the S&P 500 Index.

Liquidity. Liquidity describes the degree to which an asset or security can be quickly bought or sold in the market without affecting the asset's price.

Market maker. A dealer in securities or other assets who undertakes to buy or sell at specified prices at all times, which enables the smooth flow of financial markets. Each market maker displays buy and sell quotations for a guaranteed number of shares. Once an order is received, the market maker sells from its own holdings or inventory of those shares to complete the order.

Net asset value (NAV). The total value per ETF share of all the underlying securities in an ETF's portfolio.

Russell 2000® Index. A market-capitalization-weighted index created by the Frank Russell Co. to measure the performance of the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

S&P 500® Index. The S&P 500 Index is composed of 500 selected common stocks most of which are listed on the New York Stock Exchange. It is not an investment product available for purchase.